Lower rates, lower fees, faster closings

DON’T PUT YOUR LOAN IN DANGER.

CALL THE LOAN ARRANGER.

Lower rates, lower fees, faster closings

DON’T PUT YOUR LOAN IN DANGER.

CALL THE LOAN ARRANGER.

APPLY FOR YOUR NEW PURCHASE OR REFINANCE LOAN TODAY.

Reasons To Choose Us

With my 30+ years in the mortgage business, I have truly mastered my profession. My reputation is built around three crucial principles: discipline, determination, and integrity.

Discipline

Success isn’t measured by money or power or social rank. Success is measured by your discipline and inner peace.

Determination

Work hard. Through determination and self-focus and discipline, you can accomplish anything.

Integrity

It is true that integrity alone won’t make you a leader, but without integrity you will never be one.

Securing the Best Deal on Your New Home Loan or Refinance is Our Top Priority

MORTGAGE CALCULATOR

ABOUT ME

Hi, my name is Jason M Ruedy. With my 30+ years in the mortgage business , I have truly mastered my profession. My reputation is built around four crucial principles: words, hard work, discipline, and determination. Anybody that has ever worked with me can attest to my motivation and integrity.

When you deal with me and my carefully selected and experienced team, you will be competently guided through the loan application process. My main role is to structure files. Thanks to my extensive experience, I can look at a file and evaluate it quickly to determine what the challenges are likely to be. Ideally, the end result of any file is a successful closing, and you can be confident that I will provide you with a seamless transaction.

Jason M Ruedy

“The Home Loan Arranger“

Navigating Home Financing in Denver: Your Guide to the Best Solutions

Denver offers homeowners and investors unique opportunities in the ever-changing real estate and home financing sector. Understanding your financing alternatives is essential whether you’re moving to Colorado’s beautiful communities or expanding your investment portfolio. Due to their flexibility and customized solutions, Bank Statement Loans Colorado and leading House Mortgage Lenders in Denver are becoming more popular.

Colorado Bank Statement Loans: Homeownership Path

Traditional income verification measures no longer prevent homeownership. Bank Statement Loans in Colorado save entrepreneurs and self-employed people. These loans make buying a property in Colorado possible by using bank statements as proof of income.

Best Denver Mortgage Lenders: Trusted Partners in Homebuying

Home finance can be confusing. This is where Denver’s Best House Mortgage Lenders come in. These experts provide specialized assistance and competitive Home Buying Interest Rates to help you navigate Denver Home Financing Solutions. With their help, getting a mortgage that meets your financial goals is easy.

US investment property loans: Opportunities

US Investment Property Loans are great for real estate investors. These loans target investors buying rental homes or flipping houses. They back your investments with competitive terms and rates.

Colorado Debt Consolidation Loans: Financial Restart

Debt consolidation loans in Colorado might help with the stress of managing several bills. You can simplify payments and save on interest by combining your debts into one loan with a reduced interest rate. This financial strategy is smart for anyone seeking financial management and debt freedom.

Your Denver Real Estate Partner: The Home Loan Arranger

Denver’s thriving real estate scene centers around The Home Loan Arranger. Trust and competence make this organization a Denver Home Financing Companies leader. From Realtor Assistance for Home Buyers to Denver Real Estate Services, The Home Loan Arranger has services for first-time homebuyers and seasoned investors. Their excellent service and cheap Home Buying Interest Rates put your home financing needs in skilled hands.

A competent partner is needed to navigate Denver’s complex home financing landscape. The Home Loan Arranger will guide you through the process and provide customized solutions. Their experience makes Denver homeownership and investment success easier than ever.

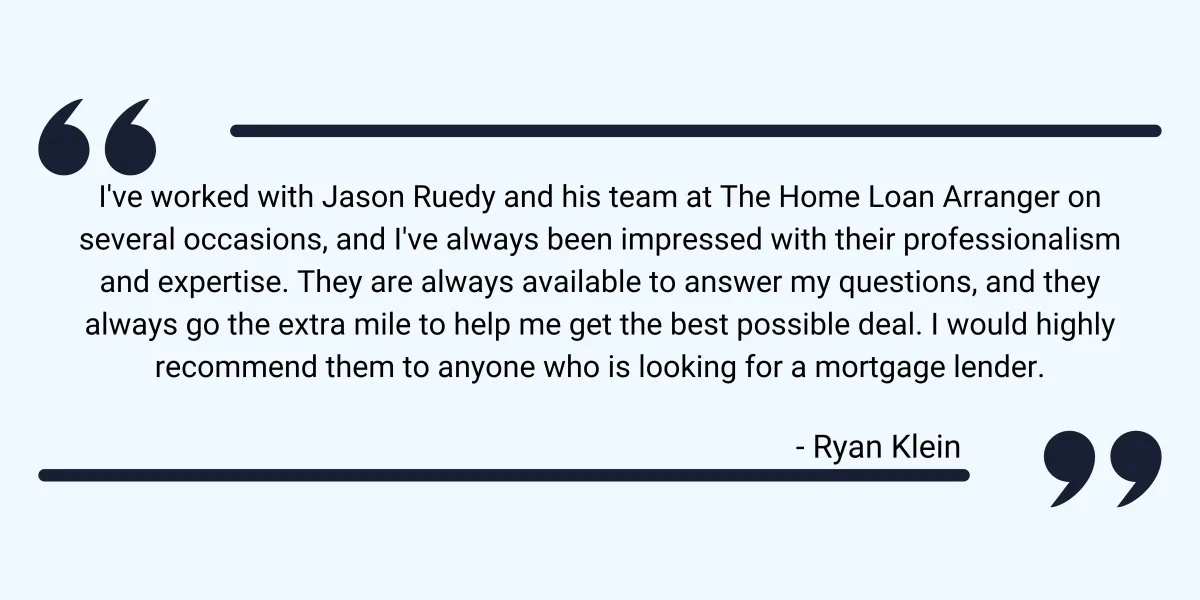

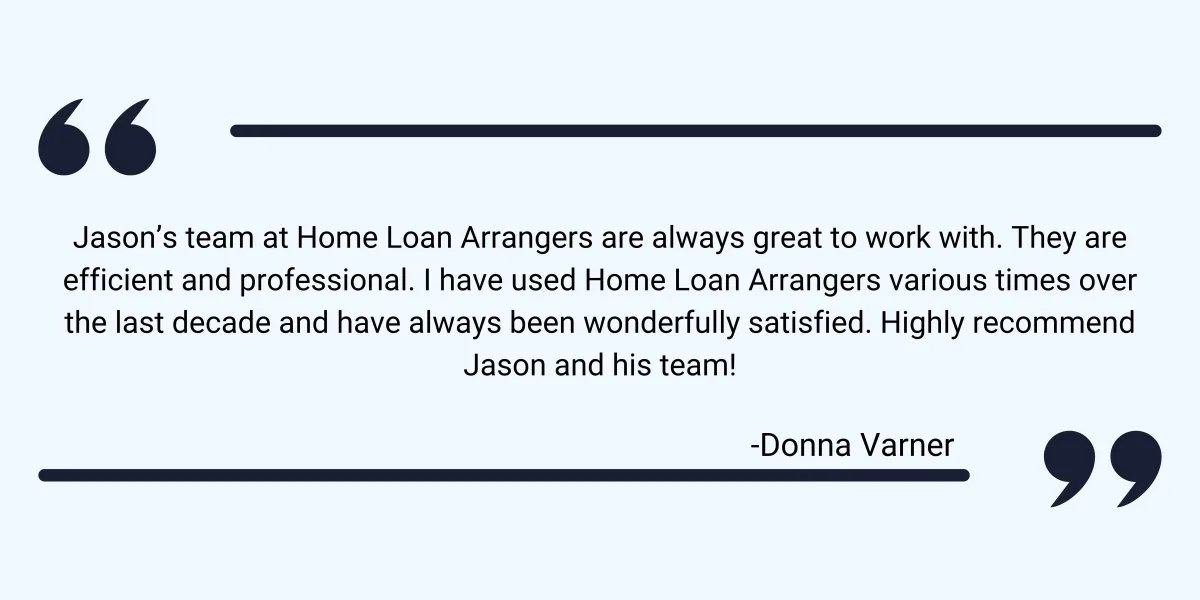

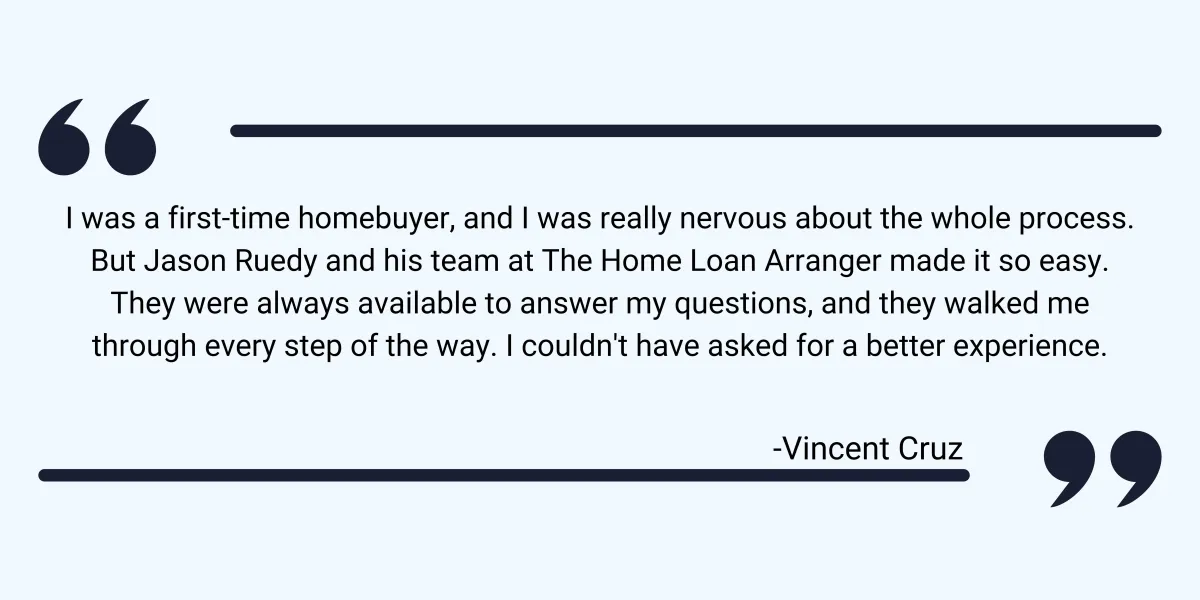

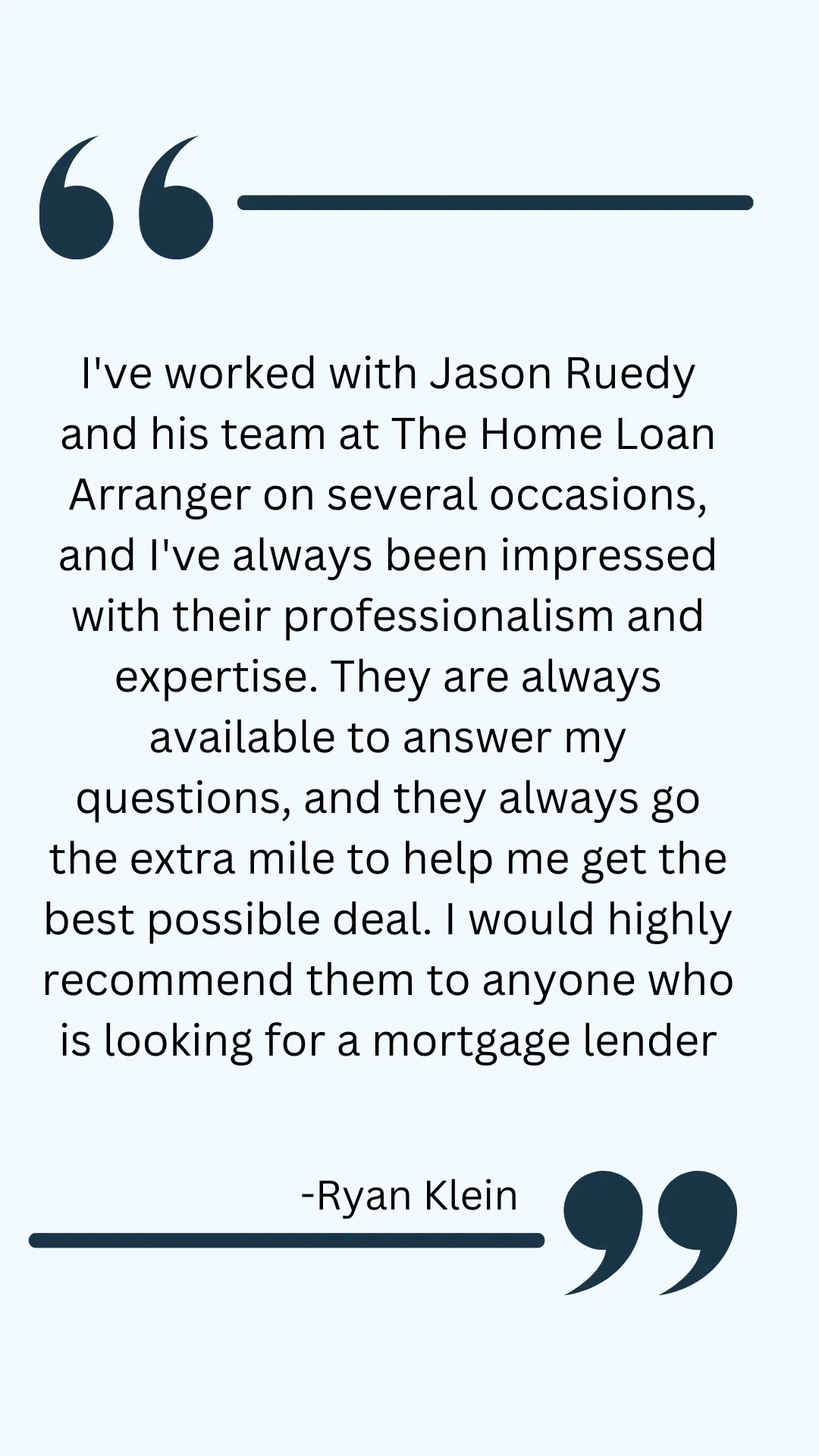

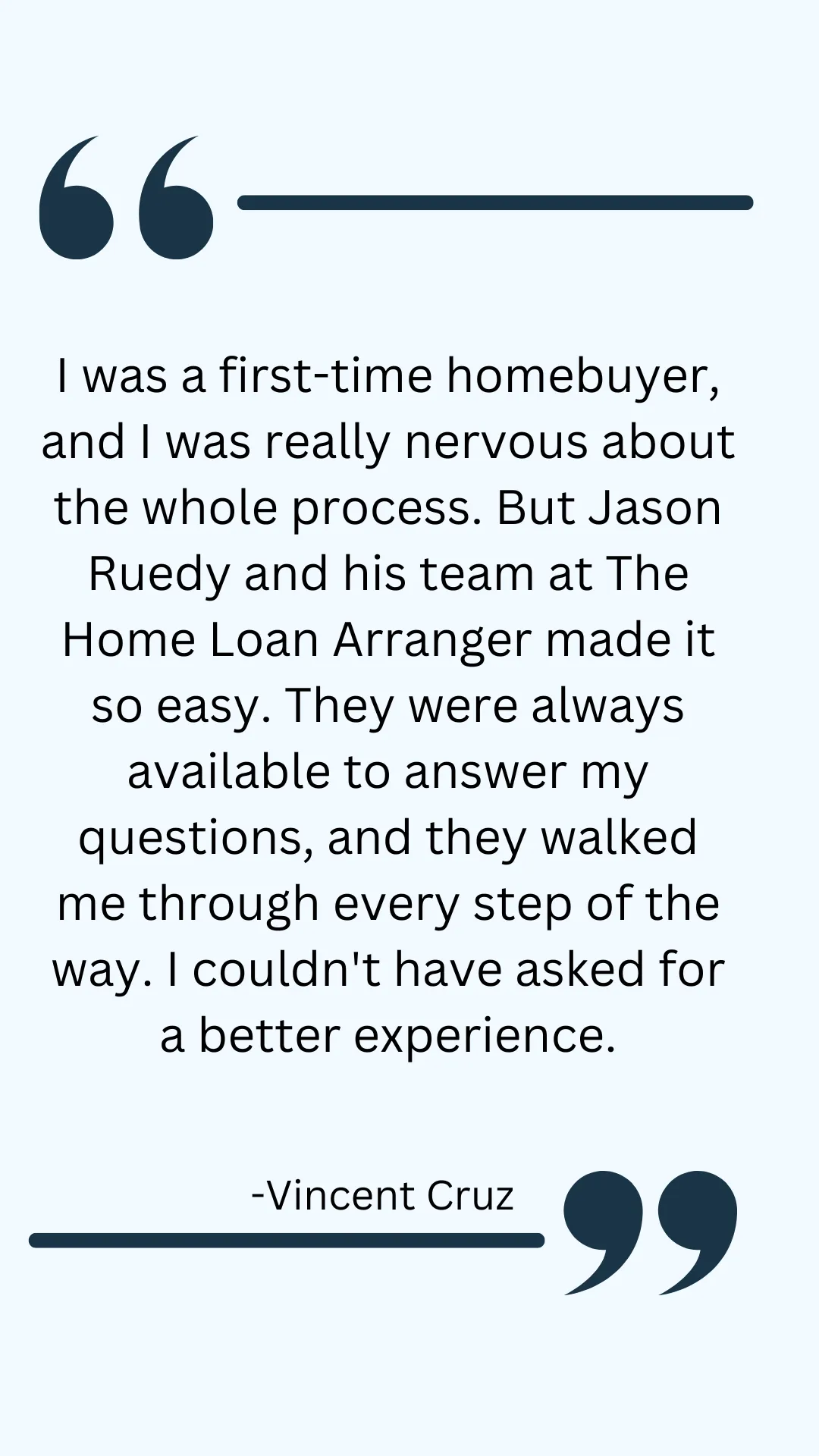

What our clients say

recent Blogs

Is Now the Time to Buy a Home in Denver? What the Recent Fed Interest Rate Cut Means for Homebuyers

Experts predict increased competition in the Denver market, so acting sooner could save you money and secure your dream home before 2025. ...more

Mortgage Trends

September 19, 2024•2 min read

How the Federal Reserve's Potential Interest Rate Cuts Could Benefit Homebuyers

With inflation cooling for the fifth consecutive month, as reported by the Labor Department, experts are anticipating that the Fed may cut rates next week, offering a glimmer of hope for those looking... ...more

Mortgage Rates ,Mortgage Savings Mortgage Trends &Home Refinance Services

September 12, 2024•2 min read

Home Ownership is More than Just a Mortgage Payment

Becoming a homeowner is a big step for people who have been renting for years or even decades. Not only is there prestige associated with being a homeowner, owning a home can also be a great investmen... ...more

Info Articles

July 24, 2024•2 min read

Contact Info

3255 S Birch St, Denver, CO 80222

Quick Links

Lower rates, lower fees, faster closings.

© Copyright 2024. The Home Loan Arranger. All rights reserved.